In-depth Review of the Australian Securities Exchange (ASX): Regulatory Compliance, Market Size, Product Structure, Internationalization, and Growth Potential

6 months before

Summary:The Australian Securities Exchange Limited (ASX) is Australia's main securities exchange, headquartered in Sydney. Founded in 2006, ASX was formed by the merger of the Australian Stock Exchange and the Sydney Futures Exchange. It is one of the most influential capital markets in the Asia-Pacific region. ASX provides stocks, bonds, ETFs, derivatives, clearing and settlement services, and is known for its strict regulation and transparency. It is regulated by the Australian Securities and Investments Commission (ASIC). Its market capitalization has always been among the highest in the world, attracting listed companies from various industries such as mining, finance, technology, and biomedicine. 📌 Full name of the company: Australian Securities Exchange Limited (ASX) 🌐 Official website: https://www2.asx.com.au 📍 Headquarters: Sydney, Australia

1. Conclusion First (Quick Overview of Key Points)

Robust supervision and clear tiers : Market and listing supervision is mainly carried out by ASIC , while systemic risk and clearing and settlement standards are supervised by the Reserve Bank of Australia (RBA); exchange self-regulatory rules are governed by the ASX Listing Rules/Operating Rules, which govern issuers and members.

Solid market size : The total market capitalization has long been in the range of AUD 2-2.5 trillion (approximately USD 1.3-1.7 trillion ), ranking first in the Asia-Pacific region.

Full product spectrum : stocks/ETFs/A-REITs/hybrid securities/warrants and ASX 24 derivatives (stock indices, interest rates, foreign exchange and commodities); clearing is handled by ASX Clear and ASX Clear (Futures) , and delivery is handled by ASX Settlement (CHESS) .

Mature internationalization path : A large number of resource and mining companies raise funds globally, and the CDI (CHESS Depositary Interests) mechanism facilitates overseas companies to trade on the ASX; there are extensive dual listings and capital connections with North American, UK and Asian markets.

Technology and governance are in the repair period : After the DLT version of CHESS replacement plan was suspended in 2022, it switched to a new route of "traditional verifiable architecture + phased launch"; compliance governance and delivery management were significantly tightened.

The investment style is clear : index finance + resources have high weights and a strong dividend culture; it has a natural ability to undertake energy transition metals, lithium/nickel/copper and carbon neutrality themes.

II. Regulatory Compliance and Investor Protection (Why “Safe and Reliable”)

Supervisor level

ASIC : Responsible for market behavior supervision, information disclosure of listed companies and market manipulation/insider trading enforcement.

RBA : Set financial stability standards for systemically important clearing and settlement facilities (CS Facilities) and conduct compliance assessments.

ASX self-regulatory rules : form an enforceable framework for listing, continuous disclosure, corporate actions, suspension and resumption of trading, market making and member compliance.

Clearing and Settlement System

ASX Clear (Cash Equities and Options CCP), ASX Clear (Futures) (Futures and Options CCP), and ASX Settlement (CHESS Settlement). We employ a "three-line defense" of margin, default funds, stress testing, and recovery mechanisms.

Investor Protection and Complaints

At the brokerage level, we implement client funds isolation, capital adequacy and compensation arrangements; investment disputes can go through the AFCA (Australian Financial Complaints Authority) channel.

Current compliance priorities

Governance reforms for the CHESS replacement, a “gradual rollout” of technology delivery, stricter change management and external independent review.

Comment : ASX's three-tier structure of "regulation + self-discipline + systematic supervision" is mature, with solid clearing centralization and delivery standardization. It is a relatively stable example between emerging and mature markets.

3. Market size and structure

Number of listed companies : Approximately 2,200+ (mainly main board, with a small number of growth board/secondary board products).

Total market capitalization : AUD 2–2.5 trillion (fluctuates with exchange rates and market conditions).

Industry weights (broad-based index caliber): Finance, resources (energy/mining), healthcare and consumer staples are the core, with the combined weight of the first two often exceeding half.

Representative indices : S&P/ASX 200 (the most mainstream benchmark), S&P/ASX 300, S&P/ASX Small Ordinaries, etc.; rich ecosystem of dividend and factor indices.

Transaction and financing : The secondary market is based on institutional and pension funds , while the activity of the primary market is related to the commodity price cycle.

IV. Product Lineage and Transaction Key Points

Stocks and Equity : Common Stock, Preferred Stock, A-REITs , Convertible and Hybrid Securities, Warrants.

ETF ecosystem : covers broad-based, industry, factor, commodity-linked, international exposure and cash management, with fast growth and a full range of categories.

Derivatives (ASX 24) :

Stock indices : The standard contract is SPI 200 (S&P/ASX 200 futures), with options and mini contracts available.

Interest rates : Bank bill/Treasury bond futures and options for hedging yield curve risk.

Commodity/Foreign Exchange related : certain energy and agricultural products, and foreign exchange related volatility hedging instruments.

Trading and settlement rhythm : Stocks are generally settled on T+2 basis; pre-market call auction, continuous auction and after-market matching are conducted in different time periods; index and interest rate futures night trading supports cross-zone trading.

5. Internationalization and Listing Channels

CDI (Depository Interest) : allows overseas registered entities to trade on the ASX in the form of CDI, retaining overseas company laws and shareholder rights, and implementing holder rights through CHESS registration.

Dual listing : There is a high frequency of dual listings for resource and biotech companies with TSX/LSE/Nasdaq/NYSE ; foreign funds and ETFs use the ASX as a gateway to provide global exposure to local investors.

Fund attributes : Primarily pensions and long-term funds, with dividend reinvestment and the dividend tax system influencing investment culture (including the refundable franking credits mechanism).

VI. Technology and Operations (CHESS Replacement and Risk Control)

Current status : The current CHESS serves as the registration and delivery backbone and has been running stably for many years. After the DLT replacement was halted in 2022, it switched to a traditional verifiable architecture with a phased replacement , emphasizing " minimum viable replacement + external audit + milestone acceptance ."

Matching and Risk Control : Low-latency matching, dynamic price fluctuation limits, circuit breakers/trading suspensions, intraday margin adjustments, stress testing, and default management systems are all available.

Operation and maintenance governance : Strengthen change management, performance regression, and capacity planning; increase independent verification of third-party suppliers and outsourcing links.

7. Suitable Investment and Usage Scenarios

Dividend and value styles : Investors who prefer stable cash flow and dividends (banks, resource leaders, A-REITs).

Commodity and resource cycles : Institutions/individuals who want to capture the lithium/copper/nickel/iron ore and LNG cycles.

Interest rate and stock index hedging : Manage asset-liability and equity positions through ASX 24 stock index and interest rate futures/options.

Foreign institutions : They need exposure to mature markets with “detailed English rules + strong clearing facilities + pension fund long-term money counterparties”.

8. Potential Risks and Constraints

Industry concentration : Finance and resources have higher weights, and structural fluctuations are more significant.

Technology replacement execution risks : The CHESS replacement project is still progressing, and the management risks of milestone delays and cost increases require continued attention.

Commodity and real estate cycles : have a significant impact on index fluctuations and financing activities.

Cross-border and competition : There is competitive pressure with US/Hong Kong stocks in terms of liquidity and valuation premium for high-growth technology and life science companies.

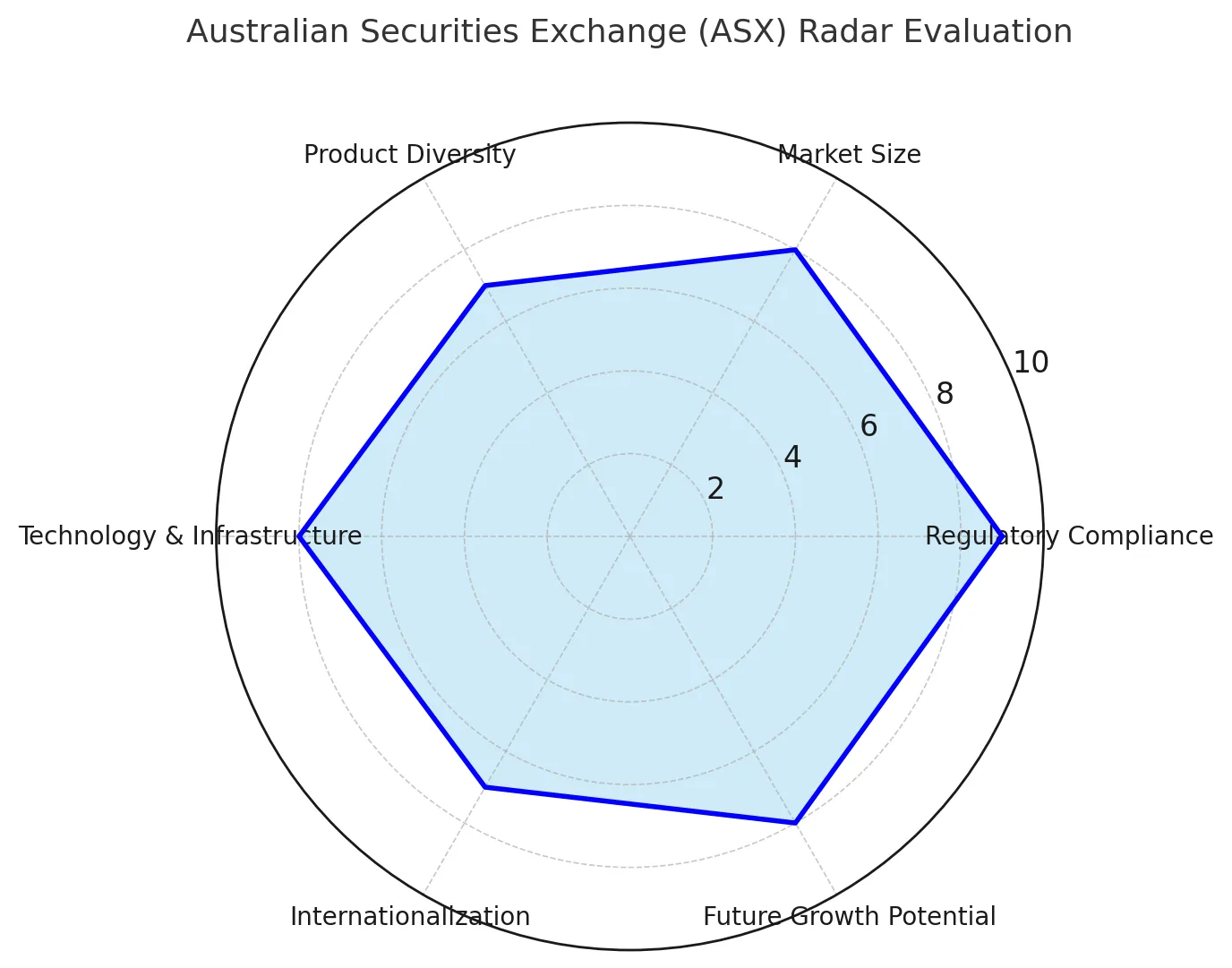

IX. Authoritative Rating (10-point scale)

Regulation & Compliance : 9.1/10 — ASIC/RBA tiered regulation with mature rules and clear enforcement; CS facilities operate in accordance with international standards.

Market Size & Liquidity : 8.3/10 - The market size is firmly in the first tier in Asia Pacific, but there is still a gap between its intraday depth and that of the US stock market.

Product Breadth : 8.8/10 – Comprehensive coverage of equities, ETFs, A-REITs, hybrid securities and ASX 24 derivatives.

Internationalization : 8.2/10 — CDI + dual listing channels are mature, and resource companies have strong global appeal.

Technology & Ops : 7.8/10 — The existing network is stable; the delivery governance and progress of the CHESS replacement period remain key areas for improvement.

Growth Potential : 8.4/10 - Energy transition metals, long-term pension funds, and structural expansion of ETFs provide medium-term momentum.

Overall rating: 8.4/10

⚠️Risk Warning and Disclaimer

BrokerHivex is a financial media platform that displays information from the public internet or user-uploaded content. BrokerHivex does not support any trading platform or instrument. We are not responsible for any trading disputes or losses arising from the use of this information. Please note that the information displayed on the platform may be delayed, and users should independently verify its accuracy.