Latest developments in the global foreign exchange market: Fluctuations in the status of the US dollar, favoring gold and non US currencies

forex8 months before

Summary:Recently, there have been a series of structural changes in the global foreign exchange market. The share of US dollar reserves has continued to decline, and although the euro has slightly rebounded, it has not become a significant beneficiary. At the same time, gold and other major currencies such as the Japanese yen and Canadian dollar are becoming the new favorites for central banks to diversify their reserves. The expectation of interest rate cuts by the Federal Reserve and the easing of the international trade situation have also driven the temporary weakening of the US dollar, prompting a profound transformation in global asset allocation and risk management. This article provides a multidimensional interpretation of the latest trends, data changes, and future risks in the foreign exchange market.

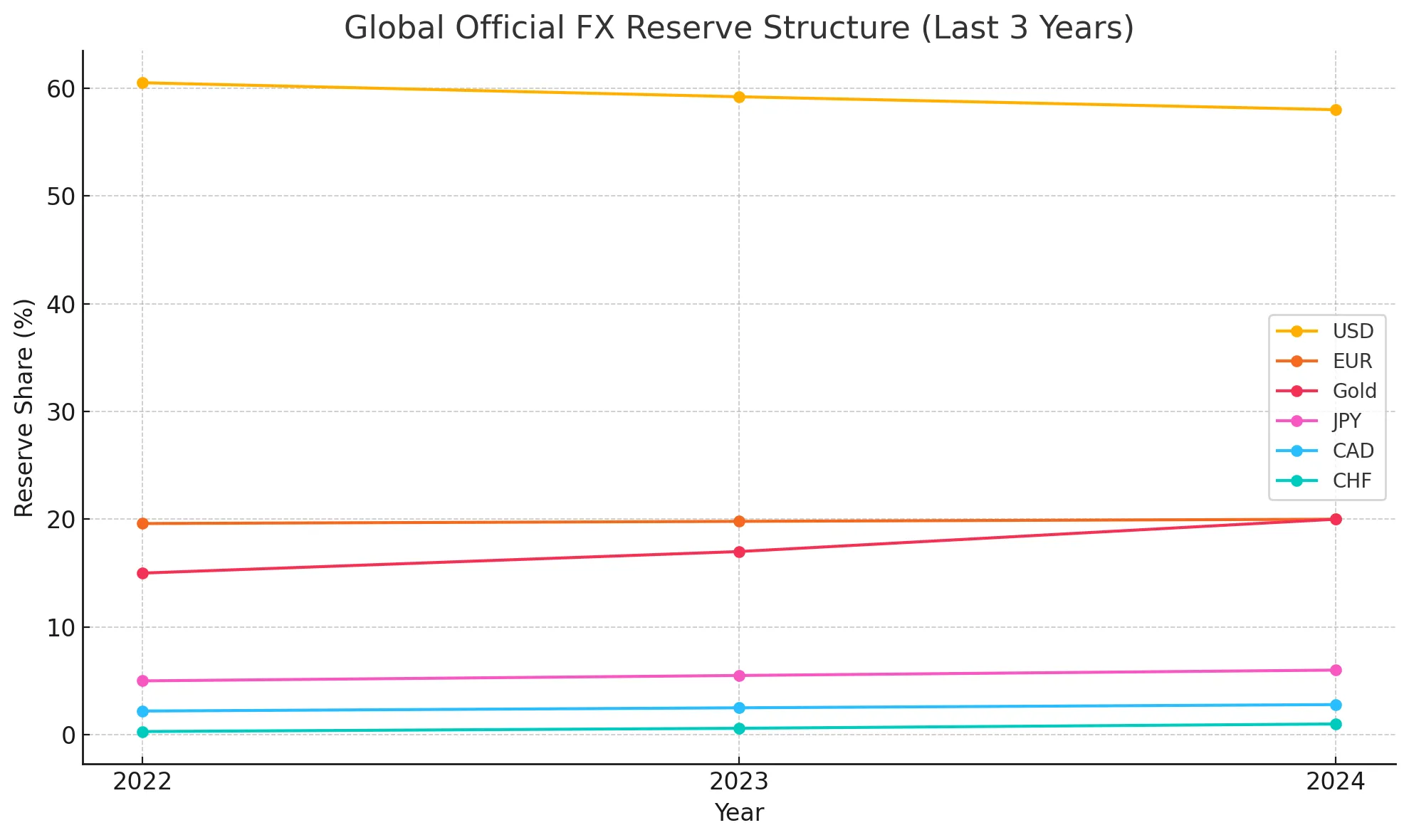

1、 The dominant position of the US dollar has loosened, and its reserve share has hit a new low in recent years. The latest data shows that as of the end of 2024, the proportion of the US dollar in global official foreign exchange reserves has dropped to 58%, the lowest level in nearly a decade. Although the US dollar remains the dominant currency in international trade and financial markets, the dependence of central banks on the US dollar is gradually weakening.

Main reason analysis: | | | Increased uncertainty in the Federal Reserve's monetary policy | |: In the past two years, the Fed's continuous interest rate hikes and high interest rate policies have put pressure on some emerging markets, prompting them to seek diversified reserve assets to reduce sensitivity to US dollar fluctuations.

Geopolitical tensions and the wave of de dollarization | | |: Geopolitical risk events such as the Russia-Ukraine conflict and Sino US trade frictions have driven some economies to accelerate de dollarization and shift to assets such as euros, yen and gold.

The worsening of the US fiscal situation has raised concerns among investors about the medium - to long-term credit of the US dollar, prompting the central bank to increase its holdings of alternative assets. 2、 The growth rate of the euro is limited, and the performance of multiple currencies and gold is impressive. Despite the decline in the share of the US dollar, the euro has not experienced significant expansion. As of the end of 2024, the proportion of the euro in global foreign exchange reserves has only slightly increased from 19.8% to 20%. This is related to the differences in fiscal policies among some countries in the eurozone and the slow progress of financial system integration, making it difficult to shake the dominant position of the US dollar in the short term.

At the same time, major currencies such as the Japanese yen, Canadian dollar, Swiss franc, and gold are rapidly gaining favor. It is worth noting that the official gold reserves of global central banks have increased to 20%, surpassing the euro for the first time in history. This reflects the central bank's strategic adjustments to combat inflation, avoid sanctions, and diversify reserve risks. 3、 The weakening of the US dollar affects global asset allocation and risk management. Since 2024, the US dollar index has fallen by about 7% cumulatively. The narrowing interest rate differential between the United States and major economies, coupled with the Federal Reserve's signal of expected interest rate cuts, has led to a structural adjustment in global capital flows.

Asset management institutions adjust their allocation | | |: Large European and American funds and pension insurance institutions increase the proportion of non US dollar asset allocation, increasing demand for currencies such as the Japanese yen and Canadian dollar. The demand for currency risk hedging has surged: Against the backdrop of intensified fluctuations in the US dollar exchange rate, fund managers have had to incorporate exchange rate risk into their daily investment decisions, leading to a continuous increase in trading volume in the foreign exchange derivatives market.

Convergence of Arbitrage Strategy | | |: With the narrowing of global interest rate differentials, traditional arbitrage trades (such as carry trades) have seen a decrease in returns, driving the market towards diversified asset allocation and active risk control.

4、 The expected easing of US China trade and interest rate cuts have intensified downward pressure on the US dollar. In mid June, the US dollar experienced a temporary correction due to the progress in US China trade negotiations and the release of easing signals from the Federal Reserve meeting minutes.

On June 12th, the US dollar fell 0.43% against the Japanese yen, while the euro rose to 1.1525 against the US dollar, reaching a seven week high. The market generally expects that if US inflation continues to fall, the Federal Reserve will initiate a rate cut cycle in the second half of the year, further intensifying the selling pressure on the US dollar. Multiple international investment banks believe in their latest outlook that the downward cycle of the US dollar may continue until mid-2025, and the trend of global foreign exchange reserve diversification is expected to further accelerate.

5、 Future prospects and risk warnings for the foreign exchange market | | Diversified reserves will become mainstream | | Gold, Japanese yen, Canadian dollar, Swiss franc, etc. will continue to be increased by central banks, and some emerging market countries will also explore new reserve assets such as digital currencies.

The requirements for foreign exchange risk management have been raised. Asset management institutions need to establish a more systematic framework for exchange rate hedging and risk control to cope with potential losses caused by intensified fluctuations in the foreign exchange market.

The Euro and regional currencies present both opportunities and challenges | | | The Euro is unlikely to shake the position of the US dollar in the short term, but with the advancement of EU financial integration, the Euro still has long-term potential. Some regional currencies such as the Chinese yuan are also expected to enhance their global influence, but the process is relatively slow due to policy barriers and liquidity restrictions. Geopolitical risks and policy adjustments need to be vigilant. External risks such as US China relations and geopolitical conflicts remain important variables affecting the trend of the foreign exchange market. Investors need to closely monitor the global macro situation and central bank dynamics.

6、 Conclusion: The global foreign exchange market is undergoing an important period of transformation. The US dollar remains strong, but its dominant position is constantly being diluted. The rise of gold and multiple currencies has provided new risk hedging and asset allocation tools for central banks and global investors. Faced with a more complex and ever-changing international financial environment, market participants can only stand undefeated in the new round of global foreign exchange games by strengthening information analysis and dynamic risk management. Author: Alex Lin

⚠️Risk Warning and Disclaimer

BrokerHivex is a financial media platform that displays information from the public internet or user-uploaded content. BrokerHivex does not support any trading platform or instrument. We are not responsible for any trading disputes or losses arising from the use of this information. Please note that the information displayed on the platform may be delayed, and users should independently verify its accuracy.