Trade data is impressive, and tariffs are beginning to show their impact

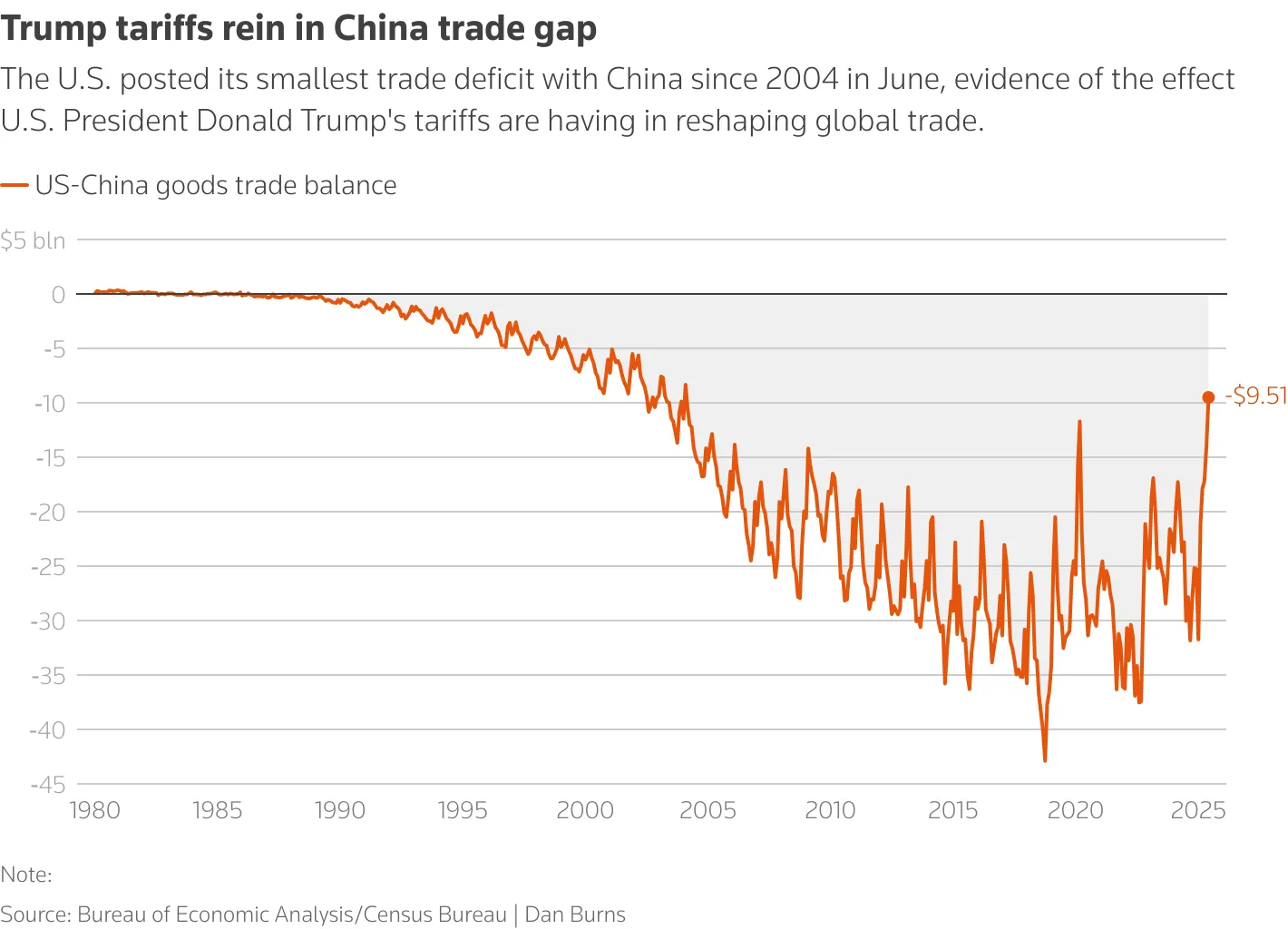

According to data from the U.S. Department of Commerce, the overall U.S. trade deficit narrowed to $60.2 billion in June 2025, a 16% decrease from the previous month, reaching its lowest level in two years [BEA, August 5, 2025]. The trade deficit with China, in particular, fell to $9.5 billion, a 70% reduction in five months, the lowest level since 2004. This structural shift stems from the new tariffs implemented by the Trump administration on August 7, covering a wide range of Chinese goods, with rates ranging from 10% to 41%. The Yale Budget Lab estimates that the average U.S. import tariff has soared from 2%-3% at the beginning of the year to 18.3%, the highest level since 1934 [Yale Estimates].

While this appears to have effectively curbed imports and the trade deficit, concerns remain about whether this is merely a superficial boom—businesses stockpiling goods and consumers delaying purchases have combined to reduce imports in the short term. Once inventories are digested, supply chains and prices could see a sharper rebound.

The service industry stagnated and economic growth momentum weakened

In contrast to the improvement in import and export data, domestic service sector activity unexpectedly cooled. According to data released by the Institute for Supply Management (ISM), the non-manufacturing PMI index fell to 50.1 in July, just above the boom-bust line and below the forecast of 51.5 [ISM, August 2025]. The employment sub-index even plummeted to 46.4, its lowest level in several months, indicating continued weakness in business hiring intentions.

Even more worrying is the resurgence of price pressures. The consumer price index rose to 69.9, a three-year high, with particularly pronounced increases in categories like home furnishings and entertainment. This suggests that the previously accumulated backlog of low-priced imported goods has been absorbed, and the true costs of tariffs are beginning to be passed on to the end market. With business plans delayed and projects shelved, the vitality of economic activity is facing challenges.

The trade surplus with China is still a tense game

Sino-US trade relations remain highly sensitive. Although the trade deficit with China narrowed significantly in June, US imports from China fell to their lowest level since 2009, at just $18.9 billion. However, this does not mean that trade tensions have eased. Last week, Chinese and US representatives met in Sweden to discuss whether to extend the August 12th deadline for negotiations, as existing tariffs could be raised again to over 100%. Trump said in an interview with CNBC, "We're very close to a deal," but markets remain cautious.

Furthermore, the US trade deficit with Canada and Germany has fallen to a five-year low, while record surpluses have been achieved with Vietnam and Taiwan, indicating that the global supply chain is quietly restructuring. However, this shift is not without cost, and the stability and cost control of alternative import routes still need time to be verified.

Data chart shows the US trade deficit with China

As structural risks emerge, how should investors respond?

While the decline in the trade deficit has supported GDP growth in the short term (annualized growth of 3.0% in the second quarter), American businesses are feeling more real operational pressures. Nationwide economist Oren Klachkin noted, "The negative effects of higher tariffs are likely to far outweigh the temporary benefits of increased policy certainty." [Nationwide report]

Investors should not focus solely on superficial data improvements while ignoring the underlying structural issues. The service sector is the primary engine of the US economy, and its triple trend of stagnant growth, declining employment, and rising prices signals potential stagflation risks. Investors are advised to monitor corporate profit warnings, end-user demand data, and the outcome of future US-China trade negotiations, maintaining flexible positions and limiting risk exposure.

The global economy is at a turning point. The truth behind the data determines your investment direction.

Want to be the first to grasp global market trends and investment opportunities? Follow us on BrokerHiveX for the latest in-depth analysis and real-time information!